Contents

- 1 Post Highlights

- 2 Standard Clothing Manufacturer Payment Terms in 2026

- 3 The 30/70 Deposit Model — How It Works

- 4 Letters of Credit — When and How to Use Them

- 5 Milestone Payment Structures for Larger Orders

- 6 Net 30 / Net 60 — Can You Get Extended Terms?

- 7 How to Protect Yourself With Advance Payments

- 8 Common Mistakes Brands Make With Manufacturer Payments

- 9 FAQ

- 9.1 What is the standard deposit for a UK clothing manufacturer?

- 9.2 Is it normal to pay 100% upfront to a clothing manufacturer?

- 9.3 When can I negotiate net 30 payment terms with a manufacturer?

- 9.4 What happens to my deposit if the manufacturer cannot complete my order?

- 9.5 Should I use a letter of credit for a UK manufacturer?

Post Highlights

- Standard UK manufacturer payment structures in 2026 — the 30/70 model, milestone payments, and when letters of credit apply

- Advance payment risk — how much is normal, what is a red flag, and how to protect deposits contractually

- The conditions under which you can negotiate net 30 or net 60 terms — and what you need to demonstrate first

- Cash flow implications of standard manufacturer payment terms for growing brands

- Five mistakes brands make with manufacturer payments — and the one that causes the most damage

Priya placed her first bulk order in March. The manufacturer asked for 50% upfront.

She paid it. Six weeks later, the factory went quiet. Emails went unanswered for nine days. When contact resumed, the explanation was vague — “supply delays.” The order arrived eleven weeks late. The deposit was never at risk, as it turned out. But Priya had no contractual protection if it had been.

Her second manufacturer asked for the same terms. This time, Priya had a written agreement specifying what the deposit covered, what triggered the balance payment, and what happened to her deposit if production did not begin within 21 days of the agreed start date.

Same payment structure. Entirely different commercial position.

Clothing manufacturer payment terms are not just about how much you pay and when. They are about what you have agreed in writing, what protections that agreement contains, and whether you have the leverage to negotiate anything beyond the manufacturer’s standard opening position.

Standard Clothing Manufacturer Payment Terms in 2026

The most common payment structure in UK clothing manufacturing is a split deposit model — a percentage paid at order placement, the balance paid at a defined trigger point before or after shipment.

| Payment Model | Structure | Typical Use Case |

|---|---|---|

| 50/50 split | 50% deposit, 50% on completion | New client relationships, first orders |

| 30/70 split | 30% deposit, 70% on shipment | Established clients, mid-volume orders |

| Milestone payments | Staged payments tied to production gates | Large orders, long production runs |

| Letter of credit | Bank-guaranteed payment on shipment | International suppliers, high-value orders |

| Net 30 / Net 60 | Full payment 30–60 days post-delivery | Long-term relationships, high trust |

| Pro forma invoice | Full payment before production begins | Very small manufacturers, first-time clients |

The 50/50 split is the default opening position for most UK manufacturers dealing with a new client. It protects the factory’s fabric procurement and labour costs against a client who does not complete the order.

The 30/70 split becomes available when a manufacturer has sufficient confidence in a client’s payment reliability — typically after two to three clean payment cycles. It improves the brand’s cash position meaningfully without significantly increasing the manufacturer’s risk.

Pro forma (full payment upfront) is a signal worth examining carefully. Some very small manufacturers operate this way legitimately. It also appears in the payment structure of fraudulent operations. A request for full payment before any production evidence exists warrants additional due diligence before transfer.

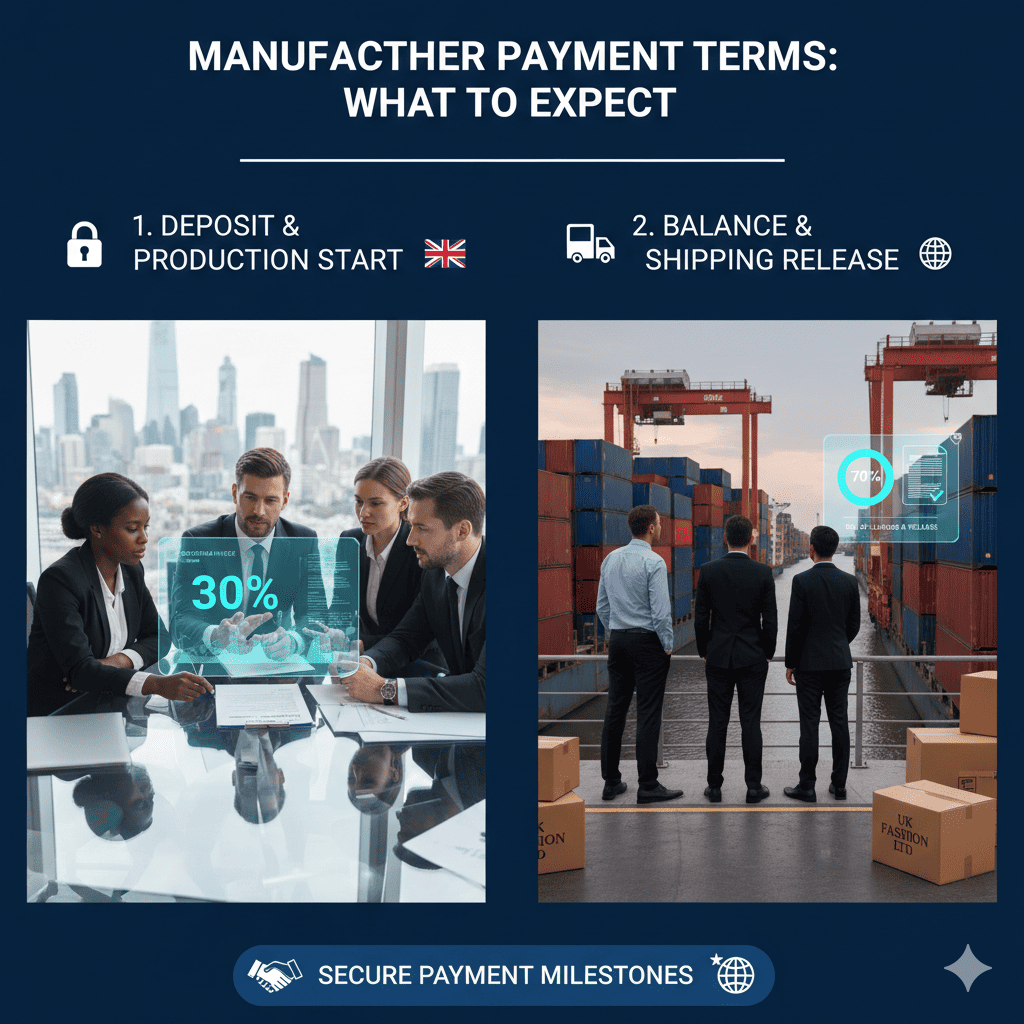

The 30/70 Deposit Model — How It Works

The 30/70 model is the most commercially balanced standard payment structure in UK clothing manufacturing. Understanding its mechanics helps you negotiate it faster.

The 30% deposit covers fabric procurement and initial floor preparation. For most garment types, fabric represents 40–60% of the total unit cost — the deposit gives the manufacturer the working capital to purchase materials without exposing their cash flow to a client default.

The 70% balance is typically due at one of three trigger points:

On shipment confirmation — payment is triggered when goods are confirmed shipped, before they arrive. Standard for established relationships with verified tracking.

On delivery — payment on receipt of goods. Preferred by brands. Resisted by manufacturers who have experienced non-payment after delivery. Achievable with a track record.

Against shipping documents — common in international production. Payment is released when the manufacturer presents a full set of shipping documents (bill of lading, packing list, commercial invoice). Provides both parties a documented trigger point.

“The 30/70 model is not about trust — it is about risk distribution. The deposit is the manufacturer’s protection. The balance trigger is yours. Negotiate both.” — Silk Routes Manufacturing Team

Priya’s second manufacturer used a 50/50 structure — standard for a new client. What she negotiated was the balance trigger: payment against shipping documents with a named freight forwarder confirmation, not on an informal notification. Same percentage split. Documented trigger. That is what contractual protection looks like in practice.

Letters of Credit — When and How to Use Them

A letter of credit (LC) is a bank-issued payment guarantee. The buyer’s bank guarantees payment to the manufacturer’s bank when specified conditions are met — typically presentation of shipping documents confirming goods have been dispatched to the agreed specification.

Letters of credit are standard in international clothing manufacturing — particularly for orders from Bangladesh, India, Turkey, and other offshore production centres where the legal recourse for non-payment is slow and expensive (Source: British Fashion Council, 2024).

For UK domestic manufacturing, letters of credit are less common but used for:

- First-time orders above £50,000 in value where neither party has an established relationship

- Orders where the manufacturer requires confirmed payment before allocating a production slot

- Situations where the brand’s payment history is unclear and the manufacturer requires bank-level assurance

The cost of a letter of credit is typically 0.5–2% of the transaction value, paid by the buyer. For large orders, this cost is justified by the protection it provides both parties. For smaller orders, the administrative overhead often outweighs the benefit.

If a UK manufacturer requests a letter of credit on a sub-£20,000 order with no stated reason, treat it as a prompt to ask why — it is an unusual requirement at that level domestically.

Milestone Payment Structures for Larger Orders

For orders above 1,000 units per style, or total order values above £30,000, milestone payment structures distribute the financial risk more evenly across the production timeline.

| Milestone | Typical Payment | Trigger |

|---|---|---|

| Order placement | 25–30% | Signed order confirmation |

| Fabric approval | 15–20% | Fabric lot approved by brand |

| Cut confirmation | 10–15% | Cutting complete, pre-production record |

| Production completion | 20–25% | Pre-shipment inspection passed |

| Delivery | Balance | Goods received in agreed condition |

Milestone structures benefit brands by tying payments to verifiable production events — you pay when something has been completed, not on a calendar basis. They benefit manufacturers by providing cash flow across a long production run rather than a single balance payment at the end.

The fabric approval milestone is worth examining specifically. Paying a tranche at fabric approval creates a formal checkpoint — you have seen and approved the actual fabric for your order before cutting begins. Brands that skip this step and pay on a calendar basis sometimes discover that the fabric cut differs from the approved swatch. A milestone payment tied to fabric approval removes that ambiguity.

Net 30 / Net 60 — Can You Get Extended Terms?

Net 30 and net 60 payment terms — where the full invoice is paid 30 or 60 days after delivery — are standard in retail and wholesale supply chains. They are rare in clothing manufacturing, and for a straightforward reason: manufacturers are not banks.

A manufacturer offering net 60 terms is effectively financing your inventory for two months. That requires a level of trust and financial stability on the manufacturer’s side that is only available to established clients with a demonstrable track record.

The conditions under which net 30 or net 60 terms become negotiable:

Minimum 18–24 months of clean payment history with the same manufacturer — not just on-time payment, but payment without disputes, corrections, or administrative complications.

Consistent seasonal volume that allows the manufacturer to plan cash flow around your payment schedule. A brand ordering once a year cannot offer the predictability that makes extended terms viable for the manufacturer.

Financial reference — some manufacturers will request a bank reference or credit check before offering extended terms. This is reasonable and should be treated as a normal part of the negotiation, not an obstacle.

Personal guarantee or director’s guarantee for smaller brands without an established credit history. Extended terms represent real credit risk for the manufacturer — they will want security that matches the exposure.

How to Protect Yourself With Advance Payments

Any advance payment without contractual protection is a commercial risk. The deposit percentage matters less than what the written agreement says about it.

The key protections to build into any manufacturing agreement before transfer of a deposit:

Production start date — the agreement must specify when production will begin following deposit receipt. If production does not begin within an agreed window (typically 14–21 days), the deposit should be refundable in full.

Deposit purpose — specify that the deposit covers fabric procurement and initial production preparation only. This prevents a manufacturer from treating your deposit as general working capital.

Refund conditions — define explicitly under what circumstances the deposit is refundable. Standard conditions: manufacturer fails to begin production within the agreed window; manufacturer cannot source agreed materials; production is abandoned by the manufacturer.

Bank transfer only — never pay a manufacturing deposit by cash, cryptocurrency, or informal transfer methods. Bank transfer creates a documented payment record that is the foundation of any dispute resolution.

Priya’s first order had none of these clauses. Her second had all of them. The payment terms were identical. The contractual position was not.

If you want to understand how Silk Routes structures payment terms with new and established clients, our clothing manufacturing services page covers our standard commercial arrangements.

Common Mistakes Brands Make With Manufacturer Payments

Paying a deposit without a written manufacturing agreement. A deposit paid on the basis of an email exchange and a verbal order confirmation is not protected by a contract. Before any money transfers, a written agreement covering order specification, payment terms, production timeline, and deposit conditions must exist.

Accepting pro forma payment terms without due diligence. Full payment before production is a legitimate structure for some manufacturers. It is also the structure used in advance payment fraud targeting new brands. Before paying pro forma to any manufacturer you have not visited, verify their registration at Companies House and request references from brands they have produced for (Source: Companies House, 2025).

Negotiating deposit percentage without negotiating the balance trigger. A brand that negotiates from 50% to 30% deposit but accepts a vague “on completion” balance trigger has improved their upfront cash position without improving their contractual protection. The balance trigger is where the real negotiation lies.

Making balance payments before pre-shipment inspection. Paying the balance before goods have been inspected removes your leverage to address quality issues. Structure balance payments to follow pre-shipment inspection sign-off, not to precede it.

Treating manufacturer payment terms as non-negotiable. A manufacturer’s opening payment position is a starting point. Established clients, large orders, and consistent seasonal volume all create legitimate grounds for renegotiation. Brands that accept standard terms indefinitely leave real commercial value on the table.

FAQ

What is the standard deposit for a UK clothing manufacturer?

The standard opening position for a new client relationship is 50% deposit at order placement, with the balance due at shipment or delivery. After two to three seasons of clean payment history, 30% deposit with 70% on shipment becomes negotiable with most UK manufacturers. The percentage matters less than what the deposit agreement says in writing about production start, refund conditions, and balance triggers.

Is it normal to pay 100% upfront to a clothing manufacturer?

Pro forma payment — full payment before production — is used by some legitimate small UK manufacturers. It becomes a red flag when combined with other signals: no physical address, no verifiable Companies House registration, no client references, or pressure to pay quickly. Before paying pro forma to any new manufacturer, visit their facility or request a video call from the factory floor. Verify their registration independently before transfer.

When can I negotiate net 30 payment terms with a manufacturer?

Net 30 terms typically become negotiable after 18–24 months of clean, consistent payment history with the same manufacturer, combined with regular seasonal ordering. Approach the negotiation with data — your payment record, total seasonal volume, and a forward plan. Net 30 is not available to new clients regardless of order size — the manufacturer has no payment history to assess the risk against.

What happens to my deposit if the manufacturer cannot complete my order?

This depends entirely on your written manufacturing agreement. Without a written agreement, deposit recovery depends on goodwill or legal action — both are slow and uncertain. With a written agreement specifying refund conditions, a deposit is recoverable if the manufacturer fails to begin production within the agreed window or cannot source the agreed materials. Always establish refund conditions in writing before transfer.

Should I use a letter of credit for a UK manufacturer?

For most UK domestic manufacturing relationships, a letter of credit is not necessary — bank transfer with a documented manufacturing agreement provides sufficient protection at standard order values. Letters of credit become relevant for first-time orders above £50,000 in value, or where the manufacturer specifically requests one as a condition of accepting the order. For international manufacturing — Bangladesh, India, Turkey — letters of credit are standard practice and worth the 0.5–2% bank fee.

For a complete guide to finding, vetting, and working with UK clothing manufacturers — including how to structure your first commercial arrangement — see our Complete Guide to Clothing Manufacturers UK.

To understand how Silk Routes structures payment terms with new and returning clients, visit about Silk Routes.

Citations and Sources

British Fashion Council — UK Fashion Supply Chain and Commercial Terms Report 2024. https://www.britishfashioncouncil.co.uk/

UKFT — UK Fashion & Textile Association: Manufacturer Commercial Standards and Guidance. https://www.ukft.org/

Companies House — UK Business Registration and Verification. https://www.gov.uk/government/organisations/companies-house

WRAP — Worldwide Responsible Accredited Production: Supplier Payment and Commercial Standards. https://wrapcompliance.org/